Week Ahead: What Are Markets Watching This Week?

Bank of Canada Widely Expected to Reduce Rates

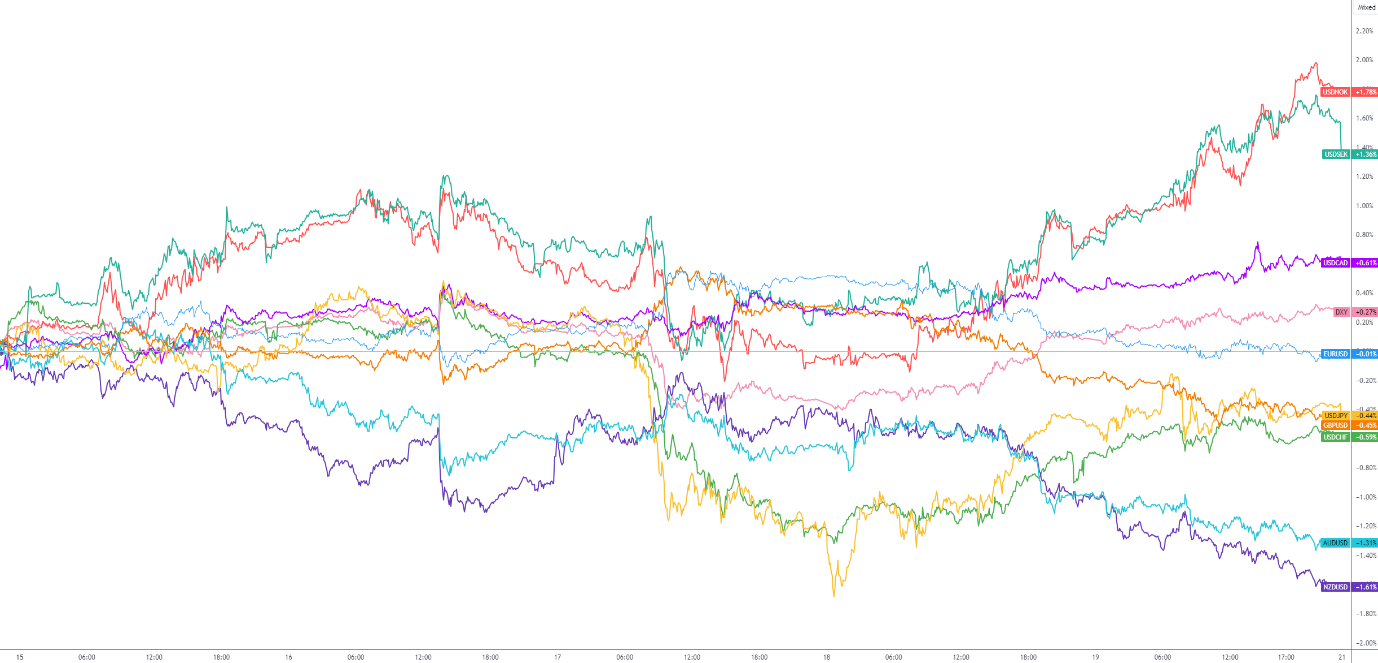

The BoC is anticipated to reduce its Overnight Policy Rate for a second consecutive meeting on Wednesday, scheduled to make the airwaves at 1:45 pm GMT. Swaps traders are now pricing in 63 basis points of easing for the year, with this week’s meeting pretty much fully priced in at this point (-24 basis points).

The BoC is anticipated to reduce its Overnight Policy Rate for a second consecutive meeting on Wednesday, scheduled to make the airwaves at 1:45 pm GMT. Swaps traders are now pricing in 63 basis points of easing for the year, with this week’s meeting pretty much fully priced in at this point (-24 basis points).

Following last week’s Consumer Price Index (CPI) inflation numbers, markets witnessed a dovish rate repricing. Contrary to markets expecting a +2.8% rise, year-on-year CPI inflation rose +2.7% in June, easing from +2.9% in May, and has been comfortably nestling within the BoC’s 1%-3% target range since the beginning of this year. Month-on-month inflation for June fell -0.1%, down from +0.6% in May, marking the first drop since late 2023. The average of the BoC’s two core measures – CPI median and trim – also slowed to +2.75% from +2.8% in May.

Labour data out of Canada also shows signs of softening, with unemployment for June rising to its highest level since the beginning of 2022 at 6.4% and employment change declining by -1,400.

In addition to the rate announcement, traders will receive the rate statement and updated Monetary Policy Report, which is released quarterly and provides an outlook of the central bank’s forecasts for growth and inflation. With the rate cut almost fully priced in at this point, a reduction will not surprise; thus, the market reaction should be limited for a cut. Attention, therefore, will shift to the central bank’s language, particularly regarding future rate reductions this year. Should the BoC strike more of a dovish tone, we can not only expect weakness in the Canadian dollar (CAD), but it may trigger growth fears in the US.

Global PMIs

Wednesday also welcomes the flash S&P Global Purchasing Managers’ Index (PMI) for the eurozone, the UK, and the US.

Wednesday also welcomes the flash S&P Global Purchasing Managers’ Index (PMI) for the eurozone, the UK, and the US.

In Europe, the eurozone PMIs will be out at 8:00 am GMT. Following the European Central Bank leaving all three of its key benchmark rates on hold last week (as well as providing little in the way of updated guidance) and inflationary pressures softening to +2.5% in June from +2.6% in May, any evidence of softness in manufacturing and services activity could strengthen the odds for a rate reduction at September’s meeting, consequently weighing on the euro (EUR). Money markets currently show a 67% probability of a cut priced in for September. Economists’ estimates indicate that the manufacturing PMI will increase to 46.1 in July from June’s reading of 45.8 (estimate high/low between 46.8 and 45.5); for the services PMI, expectations suggest a slight uptick to 53.0 in July from June’s 52.8 print (estimate high/low between 53.5 and 51.5).

Publication date: