First Light News: Divided Fed; October cut not a done deal

Good morning,

Fed Governor Stephen Miran made headlines yesterday in an interview on Bloomberg and essentially doubled down on his dovish stance. Miran noted that while he does not forecast an immediate economic contraction, he supports pre-emptive policy action to mitigate risks. Unless I have misread this, is he advocating for the Fed to adopt a more proactive forecasting role and reconsider its data-dependent stance?

You will recall that Miran dissented at the September meeting, advocating for a 50-bp rate cut, while other members opted for a more standard 25-bp cut, which is what we got. He is certainly the only one using this rhetoric right now, being the only Fed official arguing for a series of 50-bp cuts. Notably, however, more doves are becoming vocal, arguing for swifter easing, but not to the same extent as Miran.

Fed Governor Michelle Bowman supports continued rate reductions but has not endorsed Miran’s aggressive approach. We also heard from Chicago Fed President Austan Goolsbee and Kansas City Fed President Jeff Schmid yesterday, both of whom emphasised caution over excessive rate cuts amid elevated inflationary pressures.

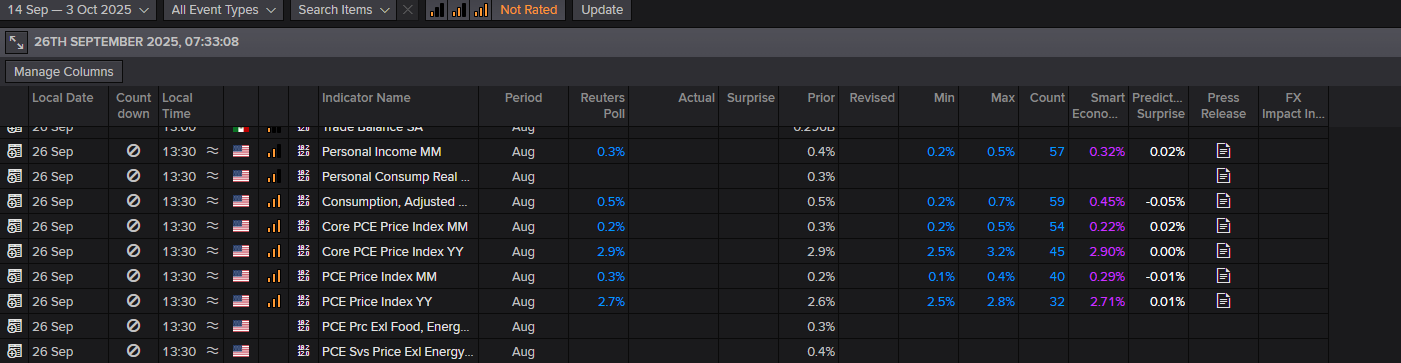

Although a modest dovish repricing was seen yesterday, with -21 bps of cuts priced in for October’s meeting and -39 bps for the year-end, the Fed is unquestionably divided; therefore, October is by no means a sealed deal in my view.

Market in a minute

The USD was bid for a second consecutive session on Thursday, adding 0.6% according to the USD Index, bolstered by a surprise upward revision to Q2 25 US GDP data. Against the EUR, the GBP, and the JPY, the buck gained 0.6%, 0.8%, and 0.6%, respectively. Interestingly, the USD Index crossed north of the 50-day SMA at 98.02, signalling the beginning of a potential uptrend.

The USD was bid for a second consecutive session on Thursday, adding 0.6% according to the USD Index, bolstered by a surprise upward revision to Q2 25 US GDP data. Against the EUR, the GBP, and the JPY, the buck gained 0.6%, 0.8%, and 0.6%, respectively. Interestingly, the USD Index crossed north of the 50-day SMA at 98.02, signalling the beginning of a potential uptrend.

US Treasury yields bear flattened yesterday following positive economic data as well as a modest hawkish repricing, hence the stronger bid at the front-end of the curve.

The S&P 500 fell by 0.5% on Thursday, marking a third consecutive session in the red and representing the longest losing streak in a month. The tariff man (Trump) is also back it seems, with pharma Stocks in particular facing pressure following announcements of 100% tariffs on branded drug imports. European pharma stocks will be closely watched today; currently, European equity futures are higher, while US equity index futures are lower.

Publication date: