First Light News: Week ahead: Middle East conflict; central bank announcements and inflation fears

Good morning,

The week that was: A geopolitical firestorm

There is no dressing it up; the past fortnight has been nothing short of extraordinary, super fluid, and very much headline-driven.

There is no dressing it up; the past fortnight has been nothing short of extraordinary, super fluid, and very much headline-driven.

What started as a military operation involving the US, Israel, and Iran has since metastasised into a global geopolitical firestorm with profound economic consequences. Brent Crude spiked to highs just shy of US$120/barrel early last week and settled around US$104, up nearly 11.3%. WTI Crude spiked to similar highs, though it concluded the week just south of US$100, up 8.8%.

The IEA described the oil shock as ‘the largest supply disruption in the history of the global oil market’, and stated that member countries are expected to release an unprecedented amount of emergency oil supply – 400 million barrels. To put this into context, this is more than double the amount of oil released in 2022 when Russia invaded Ukraine.

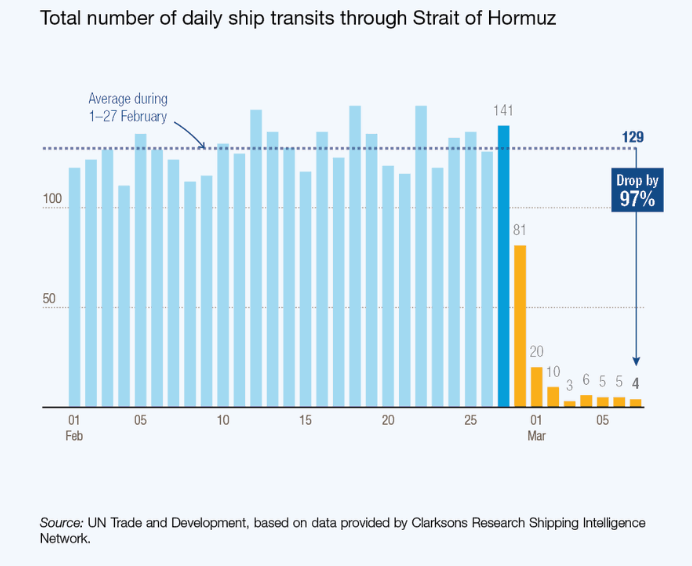

The Strait of Hormuz is key. Approximately 20% of global seaborne oil (including Gas and other refined oil products) has ground to a halt. I borrowed an image from the UN Trade and Development that demonstrates how little traffic is passing through the Strait at this point.

The duration of this war and how long the Strait remains blockaded will decide the ultimate outcome here. Naturally, recession calls have increased, and the longer this conflict lasts, the worse it will be for the economy.

Last Friday’s data delivered a clear message: stagflation. According to the BEA’s second estimate (preliminary), US Q4 25 GDP growth cooled to 0.7% – down from 1.4% in the first estimate – and US January PCE inflation remained elevated with headline and core at 2.8% and 3.1%, respectively. However, while the government shutdown in Q4 reduced spending and influenced GDP, and although we will likely see a bounce-back in growth in Q1 26, the economy’s trajectory is unquestionably trending lower. The combination of elevated prices and lower growth should keep the Fed on the sidelines this week.

The week that is: Geopolitics and central banks in focus

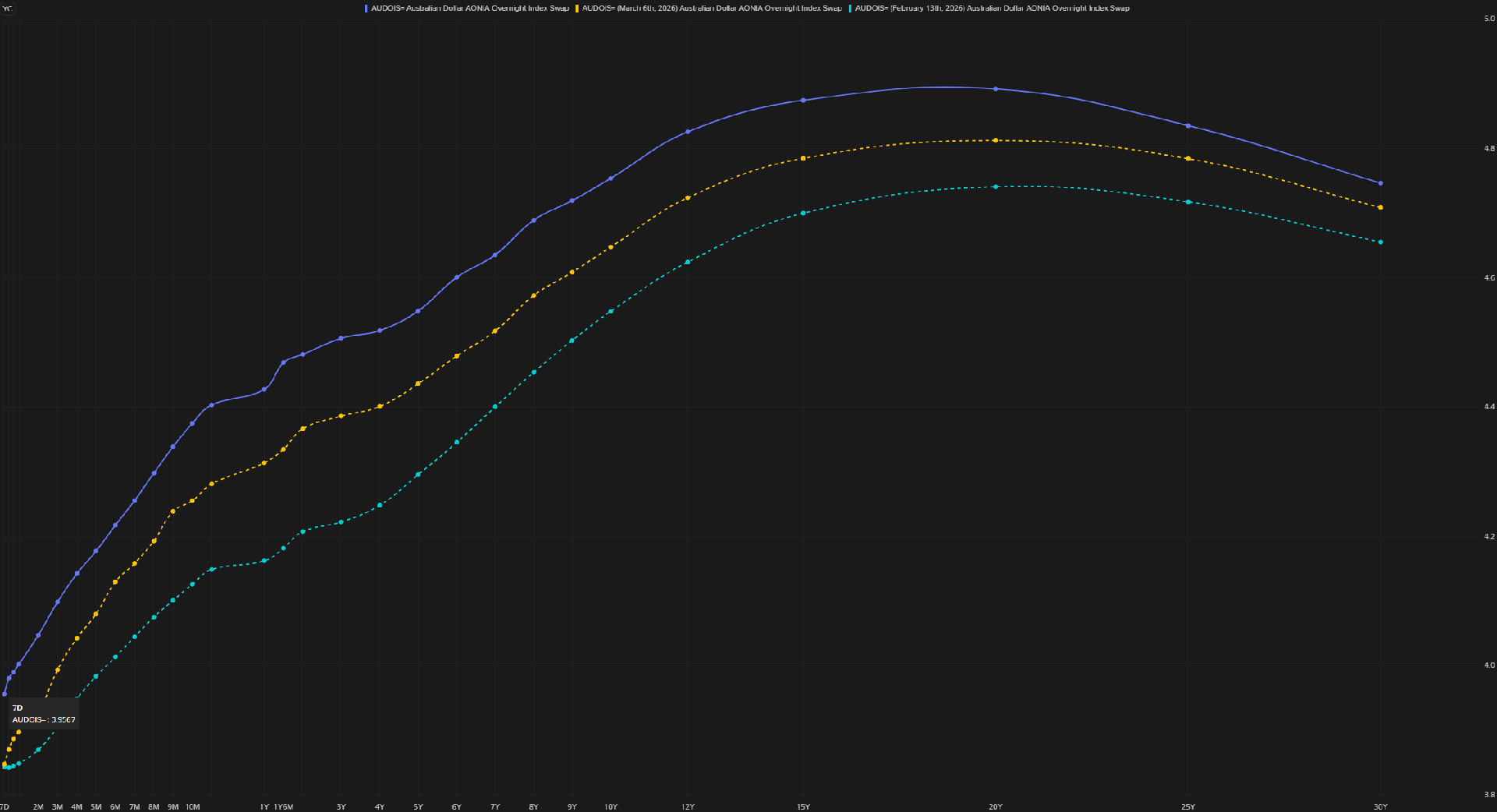

Although geopolitics remains top of mind for investors this week, seven key central bank announcements will share the spotlight. Tuesday features an update from the RBA, while Wednesday includes meetings from the BoC and the Fed. Thursday will see the BoJ, the SNB, the BoE, and the ECB. However, six of these seven central banks are widely expected to keep policy rates steady.

Although geopolitics remains top of mind for investors this week, seven key central bank announcements will share the spotlight. Tuesday features an update from the RBA, while Wednesday includes meetings from the BoC and the Fed. Thursday will see the BoJ, the SNB, the BoE, and the ECB. However, six of these seven central banks are widely expected to keep policy rates steady.

Publication date: