Forex market analysis: 8 January 2025

Today’s session is pivotal in shaping the market’s direction for the remainder of the week. Stay tuned and stay informed.

KEY INDICATORS

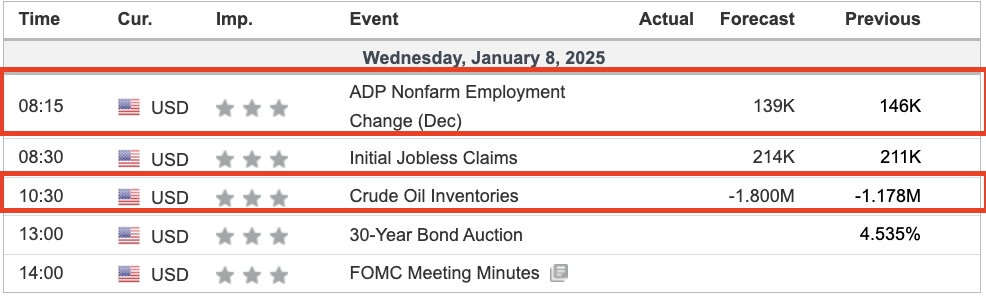

US labour market spotlight

US labour market spotlight

- Today’s focus is on the ADP Employment Report for December, a critical indicator ahead of Friday’s Non-Farm Payrolls release.

- This report will provide insights into private-sector job growth and its implications for Federal Reserve policy in the coming months.

- This report will provide insights into private-sector job growth and its implications for Federal Reserve policy in the coming months.

Global market sentiment

- Asia: Asian markets ended mostly higher, buoyed by optimism around China’s trade data, which showed signs of recovery despite lingering global headwinds.

- Europe: European stocks opened mixed as investors assessed new inflation data and corporate updates ahead of tomorrow’s European Central Bank (ECB) meeting minutes.

- Asia: Asian markets ended mostly higher, buoyed by optimism around China’s trade data, which showed signs of recovery despite lingering global headwinds.

- Europe: European stocks opened mixed as investors assessed new inflation data and corporate updates ahead of tomorrow’s European Central Bank (ECB) meeting minutes.

Oil prices and energy markets

- Crude oil prices are holding steady after recent gains, supported by supply constraints and signals of demand recovery.

- Energy stocks remain in focus as the latest US crude inventory report is due today.

- Crude oil prices are holding steady after recent gains, supported by supply constraints and signals of demand recovery.

- Energy stocks remain in focus as the latest US crude inventory report is due today.

MARKET MOVERS

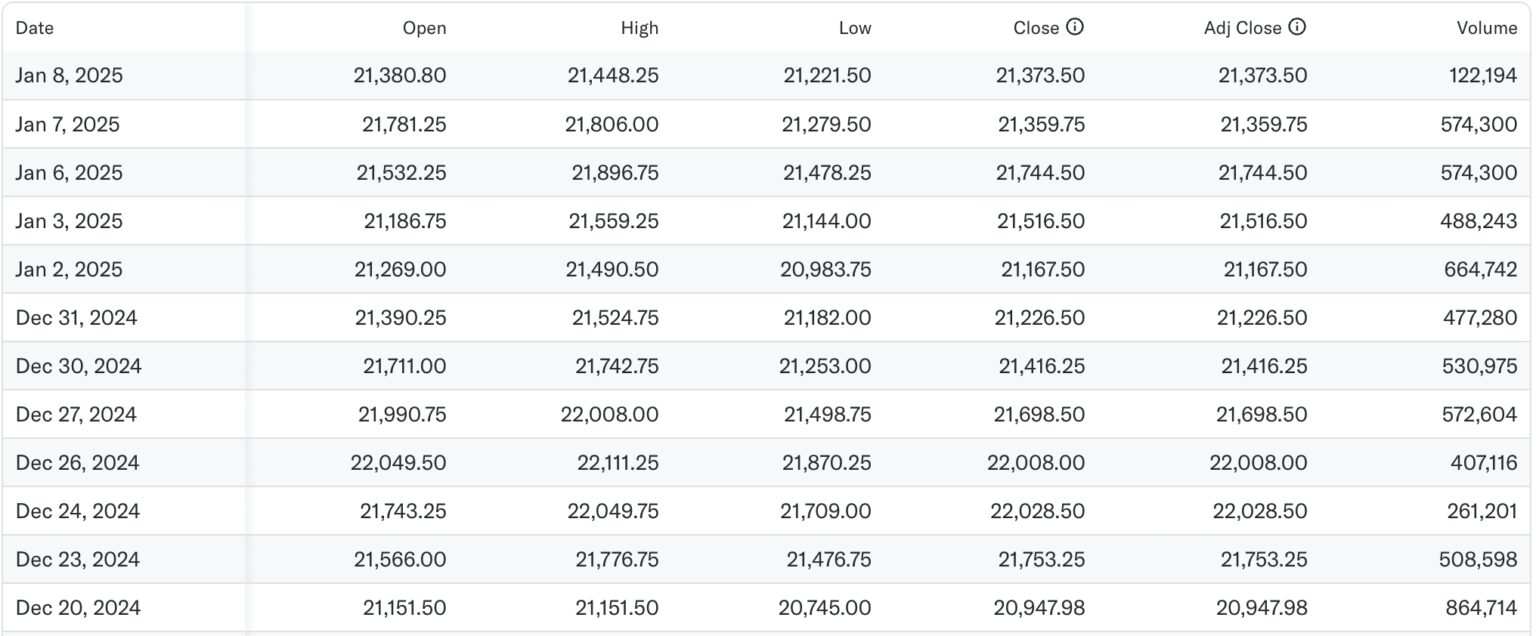

Nasdaq100

Nasdaq100

Possible short preference

Short positions below 21058.78 with targets at 20973.11 & 20905.80 in extension.

Alternative scenario

Above 21209.73 look for further upside with 21268.89 & 21317.84 as targets.

The RSI is below its neutrality area at 50%, falling the most as it shed 1.89%, or 375 points.

Short positions below 21058.78 with targets at 20973.11 & 20905.80 in extension.

Alternative scenario

Above 21209.73 look for further upside with 21268.89 & 21317.84 as targets.

The RSI is below its neutrality area at 50%, falling the most as it shed 1.89%, or 375 points.

Inflation fears drag down US markets

- US stocks fell, and Treasury yields rose on Tuesday as the ISM Services Index showed a significant jump in prices for December.

- Asia-Pacific markets traded mixed on Wednesday. South Korea’s Kospi rose by 1.3%, boosted by shares of Samsung Electronics, which climbed around 3.6%, even as the company forecast that its fourth-quarter profits would fall short of LSEG expectations.- The price index for December’s ISM report jumped to 64.4% from 58.2% in November, representing an increase of more than 10%.- It’s the first time since January 2024 that the reading has come in above 60%.

- US stocks fell, and Treasury yields rose on Tuesday as the ISM Services Index showed a significant jump in prices for December.

- Asia-Pacific markets traded mixed on Wednesday. South Korea’s Kospi rose by 1.3%, boosted by shares of Samsung Electronics, which climbed around 3.6%, even as the company forecast that its fourth-quarter profits would fall short of LSEG expectations.- The price index for December’s ISM report jumped to 64.4% from 58.2% in November, representing an increase of more than 10%.- It’s the first time since January 2024 that the reading has come in above 60%.

Publication date: