First Light News: Stocks & Bonds down; Gold at all-time highs!

Good morning,

As both Equity and Bond markets retreated in synchronised fashion yesterday, the 60/40 portfolio allocation strategy faces challenges. The S&P 500 fell 0.7% to 6,415, the Nasdaq 100 dropped 0.8% to 23,231, with the Dow Jones Industrial Average shedding 0.6% to 45,295.

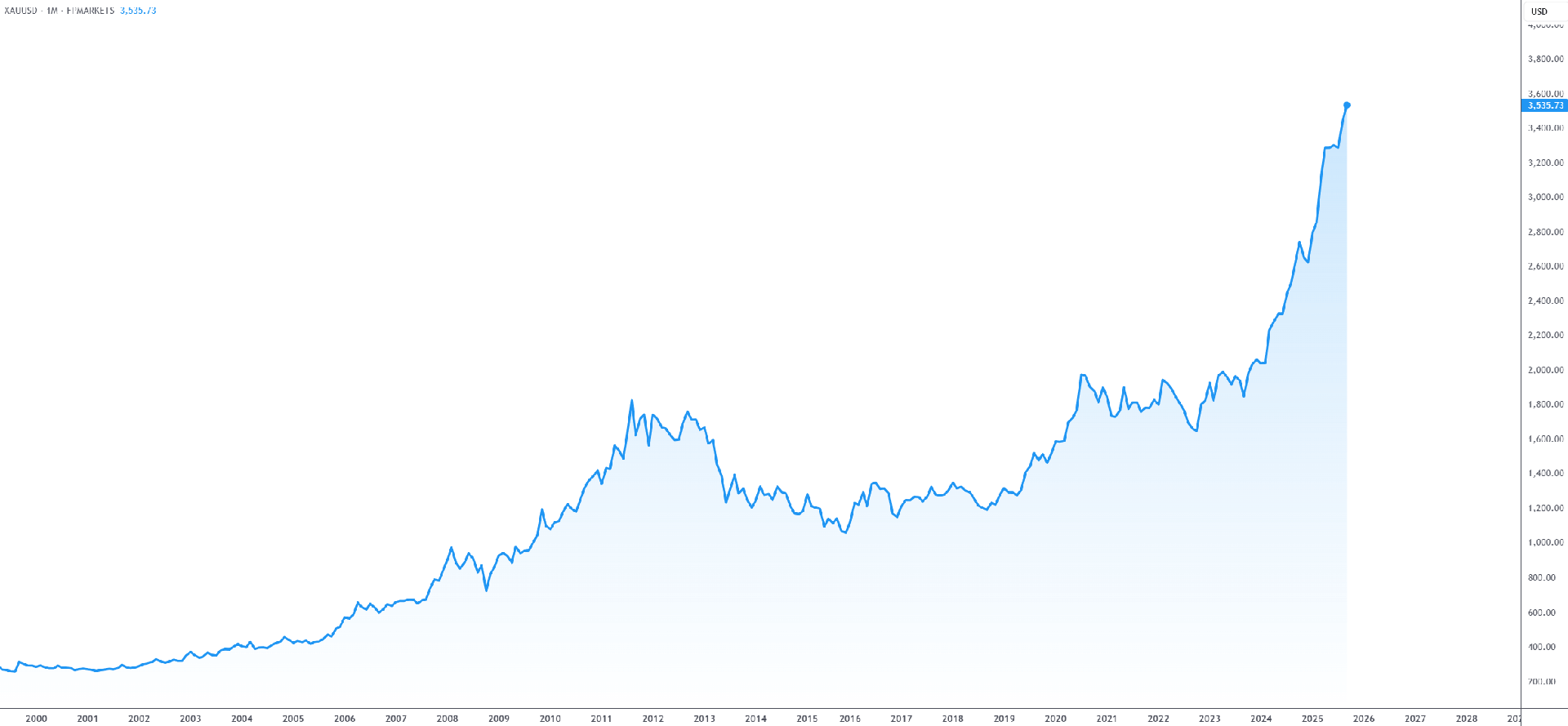

On a more positive note, Spot Gold (XAU/USD) surged to fresh all-time pinnacles yesterday, peaking at US$3,546. As you can see below, it is quite the chart! The precious metal’s rally beyond $3,500 signals a fundamental recalibration of risk perception, underpinned by central bank accumulation, expected policy easing from the US Federal Reserve (Fed), uncertainty surrounding Fed Governor Lisa Cook, as well as global tariffs, and, of course, persistent geopolitical tensions have coalesced to drive institutional and retail demand.

Bond rout deepens

The bond market is fairly quiet this morning; however, yesterday was anything but, with investors continuing to price in a higher term premium.

The bond market is fairly quiet this morning; however, yesterday was anything but, with investors continuing to price in a higher term premium.

Global long-duration debt stress arises from elevated government borrowing, high debt levels, and political instability. For example, political turmoil in France, the UK, and Japan, as well as increased expenditure in Germany, raises doubts about fiscal health and governments’ ability to address their debt. Ultimately, the bond market is telling us that it is concerned about the current situation.

The FP Markets Research Team released a brief note on the UK bond market yesterday, showing that the ‘yield on 30-year borrowing costs reached an eye-popping level of nearly 5.700%, breaching thresholds not witnessed since 1998 and marking a watershed moment for UK sovereign debt markets. Concurrently, the yield on the 10-year note jumped to a high of 4.806%, inching closer to 4.815% – a level that, on several occasions, has prompted bond buying since this year’.

It was also a particularly busy day in other UK markets. In addition to bonds selling off, which places GILT yields north of Liz Truss’ mini-budget debacle, Equities took a substantial hit. This was evident across mid-cap Stocks – the FTSE 250 dropped more than 2.0% on the day, while the benchmark FTSE 100 ended lower by 0.4%. The British pound (GBP) also navigated deeper waters, down 1.1%, and is moderately on the back foot in early European trading this morning.

Publication date: