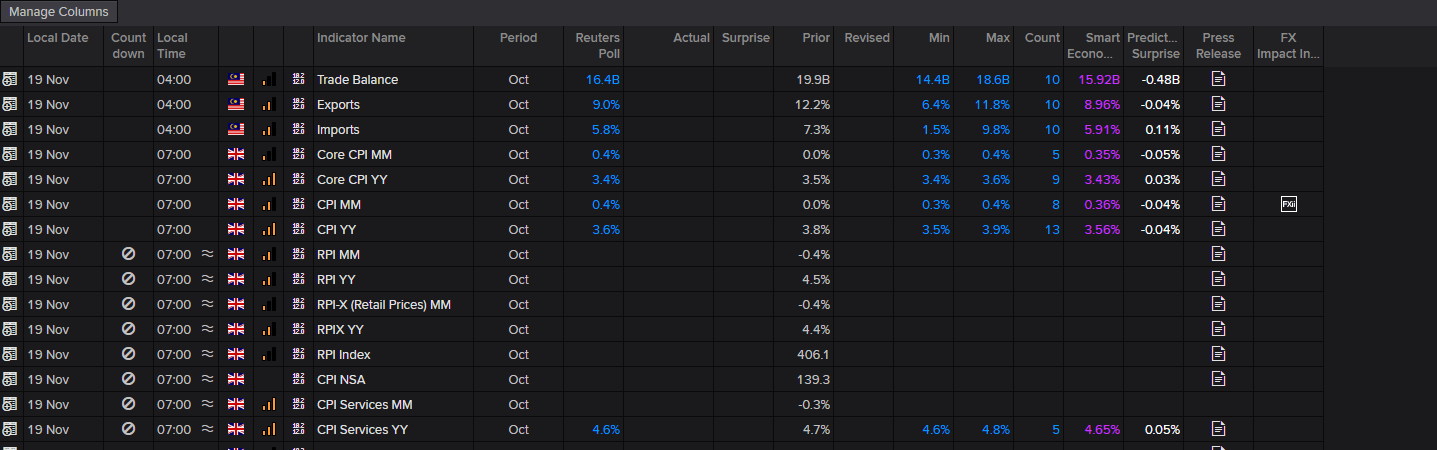

First Light News: Week Ahead: US government reopening brings September data!

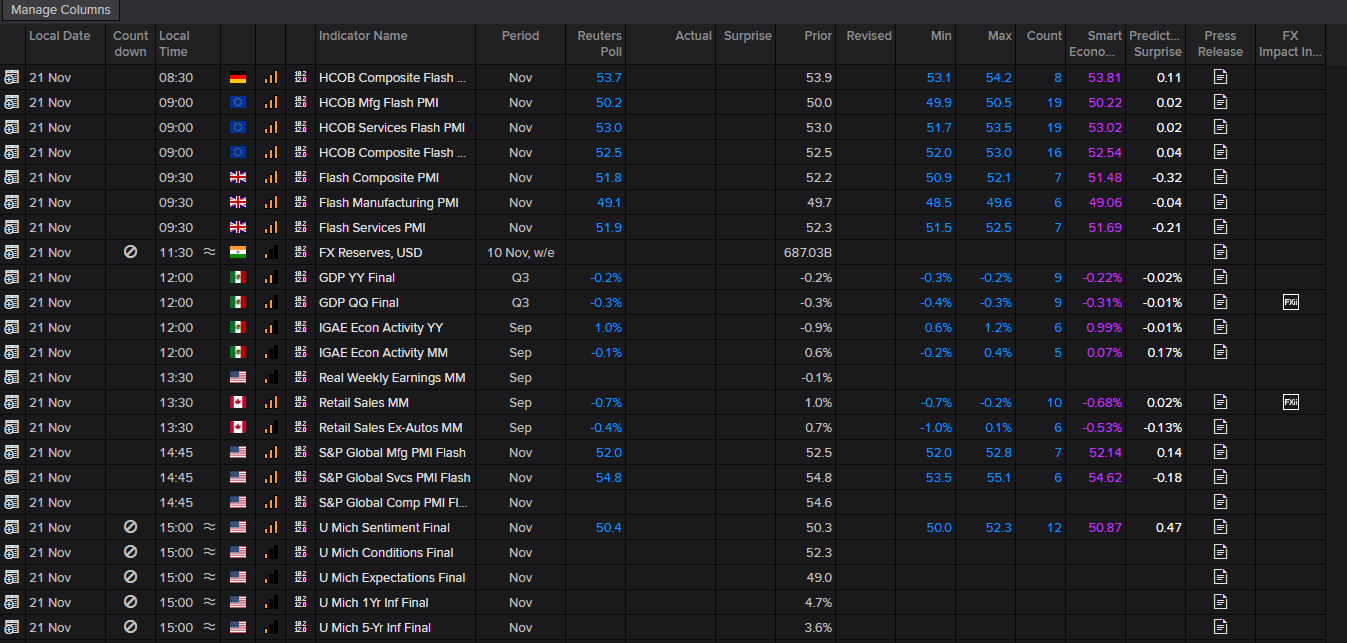

Markets welcome what could be a pivotal week, as they grapple with the aftermath of the prolonged US government shutdown. The week’s highlights will include the delayed September US jobs report on Thursday, UK inflation numbers, and S&P Global PMI data.

So, the day finally arrived. After shutting its doors at the beginning of October and keeping things bolted down for a record 43 days, the US government reopened and, with it, should follow outstanding economic data. As I am sure you can imagine, despite private-sector data, the absence of official economic figures has left the Fed – and market participants, for that matter – in the dark.

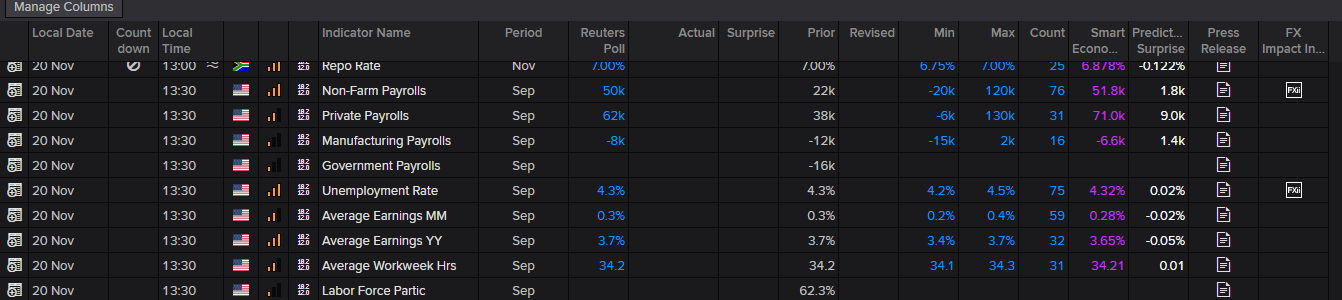

September US jobs report in focus

The September jobs report will be released this week; the data was collected before the shutdown, but not processed. Therefore, this should be reasonably straightforward to publish. This follows both ISM and ADP prints that echo a soft jobs market, with this week’s payrolls data forecasting 50,000 new jobs (up from 22,000 in August), and the unemployment rate expected to remain unchanged at 4.3% (per LSEG calendar below).

The September jobs report will be released this week; the data was collected before the shutdown, but not processed. Therefore, this should be reasonably straightforward to publish. This follows both ISM and ADP prints that echo a soft jobs market, with this week’s payrolls data forecasting 50,000 new jobs (up from 22,000 in August), and the unemployment rate expected to remain unchanged at 4.3% (per LSEG calendar below).

The October employment release, on the other hand, will be trickier. The payroll number should be reasonably straightforward, as it is derived from the Establishment survey. However, the unemployment rate will unlikely be included in the report, as this forms part of the Household survey, which requires calling households, which has not been done.

Should we see a meaningfully soft jobs print this week, one that sees payrolls drop into negative territory, could prompt USD downside and increase rate-cut bets – potentially extending USD weakness to the 50-day SMA at 98.57 on the USD index.

You may recall that we recently saw a notable hawkish repricing in Fed rate expectations amid neutral-to-hawkish Fed commentary, with investors now assigning only a 40% chance of a rate cut (down from 70% a week ago). However, the USD declined, and Gold was bid, which is not the typical price action you would expect having seen a rather large repricing, suggesting more complex forces are at play beyond simple monetary policy arithmetic.

We will also get the Fed minutes from the previous meeting. However, I do not see much value in this release, as it predates the end of the shutdown.

Publication date: