Week ahead: All about the August US jobs data!

In a holiday-shortened week, all eyes will be on the August US jobs report, particularly after July’s release raised questions.

July’s employment report painted a sobering picture, with a mere 73,000 positions added to the US workforce – a figure that fell markedly short of expectations and represented a pronounced deceleration from the momentum seen in June. Interestingly, this was also the first softer-than-expected payroll print since March.

However, you will recall that it was the chunky downward revisions that raised eyebrows, with May and June revised lower by 258,000 payrolls (May was revised lower by 125,000 from 144,000 to 19,000, and June was revised down by 133,000, from 147,000 to 14,000). Accompanying these meagre revisions was the 3-month average of just 35,000 payrolls, reflecting a considerably slower pace of hiring in the US.

On the back of the July figures, this resulted in US President Donald Trump firing the Commissioner of the Bureau of Labor Statistics, Erika McEntarfer, after he claimed the jobs data were ‘rigged’ to make the Republicans, and himself, look bad. In my view, Trump overstepped the line here. Although I hold no political bias whatsoever, he did a good job of making himself ‘look bad’ after firing McEntarfer, as I believe she has no influence over the final payroll figures. All he achieved was to undermine trust in a very important economic data point.

Economists expect subdued payroll growth in August

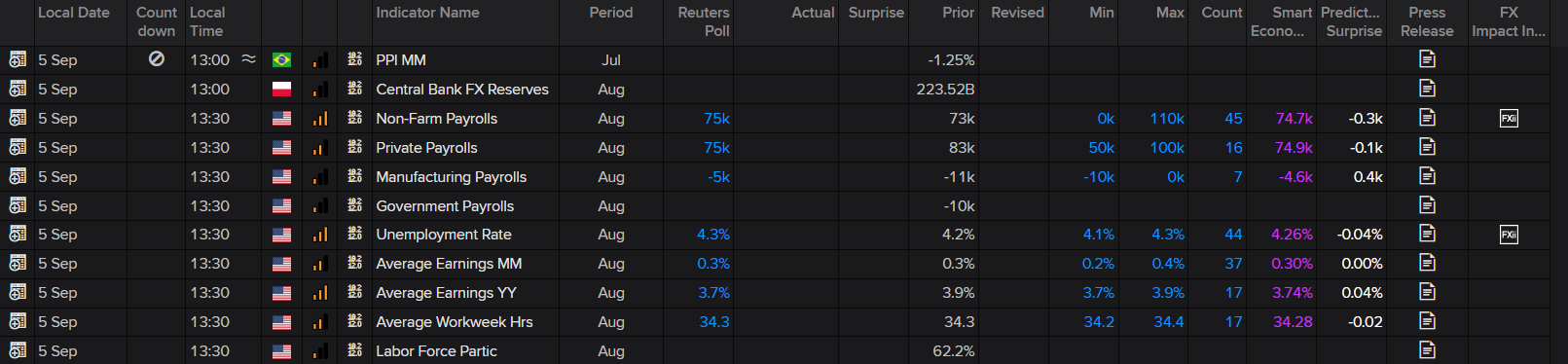

Economists expect August payrolls to remain subdued at 75,000, down from 73,000 in the previous month (LSEG data – below). The forecast distribution for the release ranges from a high of 110,000, as projected by Deutsche Bank, to a low of 0, according to Scotiabank.

Economists expect August payrolls to remain subdued at 75,000, down from 73,000 in the previous month (LSEG data – below). The forecast distribution for the release ranges from a high of 110,000, as projected by Deutsche Bank, to a low of 0, according to Scotiabank.

In terms of private payrolls, analysts are also expecting a softened print of 75,000, down from 83,000. The unemployment rate is forecast to have increased to 4.3%, from 4.2%, and wages are expected to have remained steady at 0.3% MM, though eased to 3.7% (from 3.9%) YY.

LSEG data

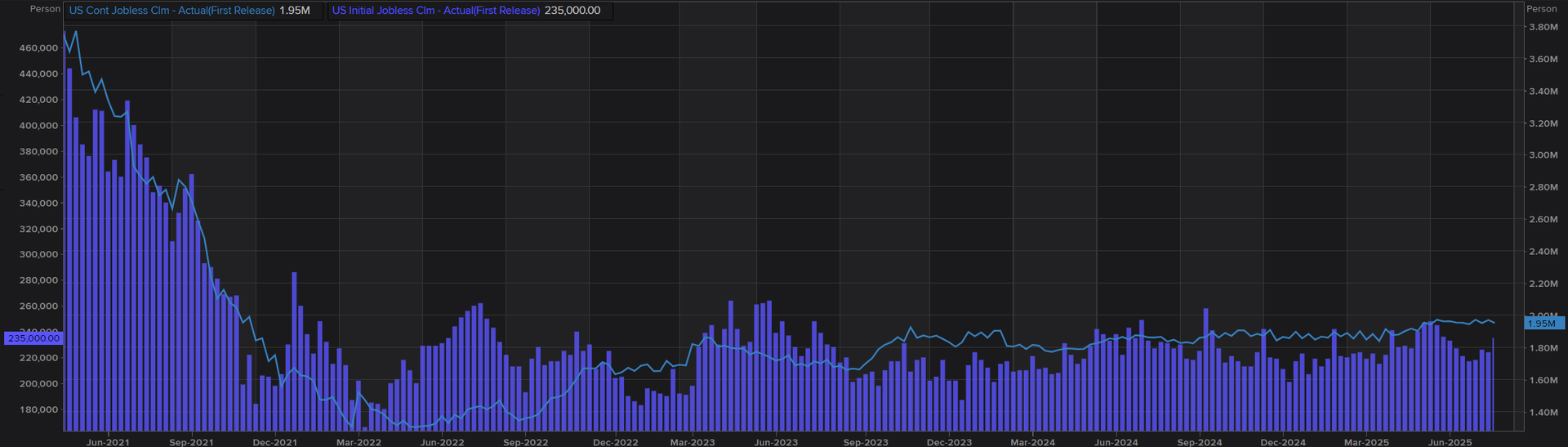

These estimates align with recent comments from Federal Reserve (Fed) officials, which highlighted that the US is in a ‘low hire, low fire’ mode. Additionally, this aligns with weekly jobless claims data. As shown on the chart below, although marginally off lows, unemployment claims are not signalling any red flags that suggest widespread layoffs. Continuing job claims further reinforce this picture, trending higher since bottoming out in 2022 and indicating that it is now proving more difficult to find employment.

Publication date: