First Light News: It’s NFP Day!

Good morning,

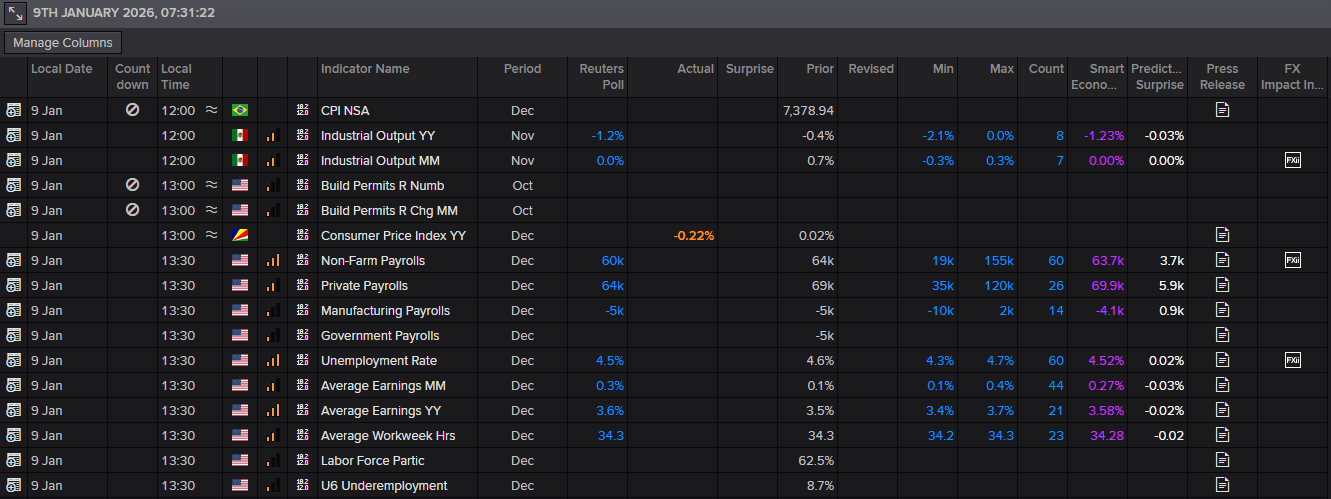

Markets are on tenterhooks – today is all about the December US employment report, which is the last jobs print for 2025. This should provide a cleaner view of the labour market and help determine the trajectory of Fed easing and the USD.

The stakes are high following delayed October and November data, along with a mixed bag of jobs figures released this week, and the Fed reducing rates by 75 bps at the tail end of last year to 3.50%-3.75%. Today’s numbers should help answer whether the jobs market has stabilised.

Economists expect the US economy to have added 60k jobs

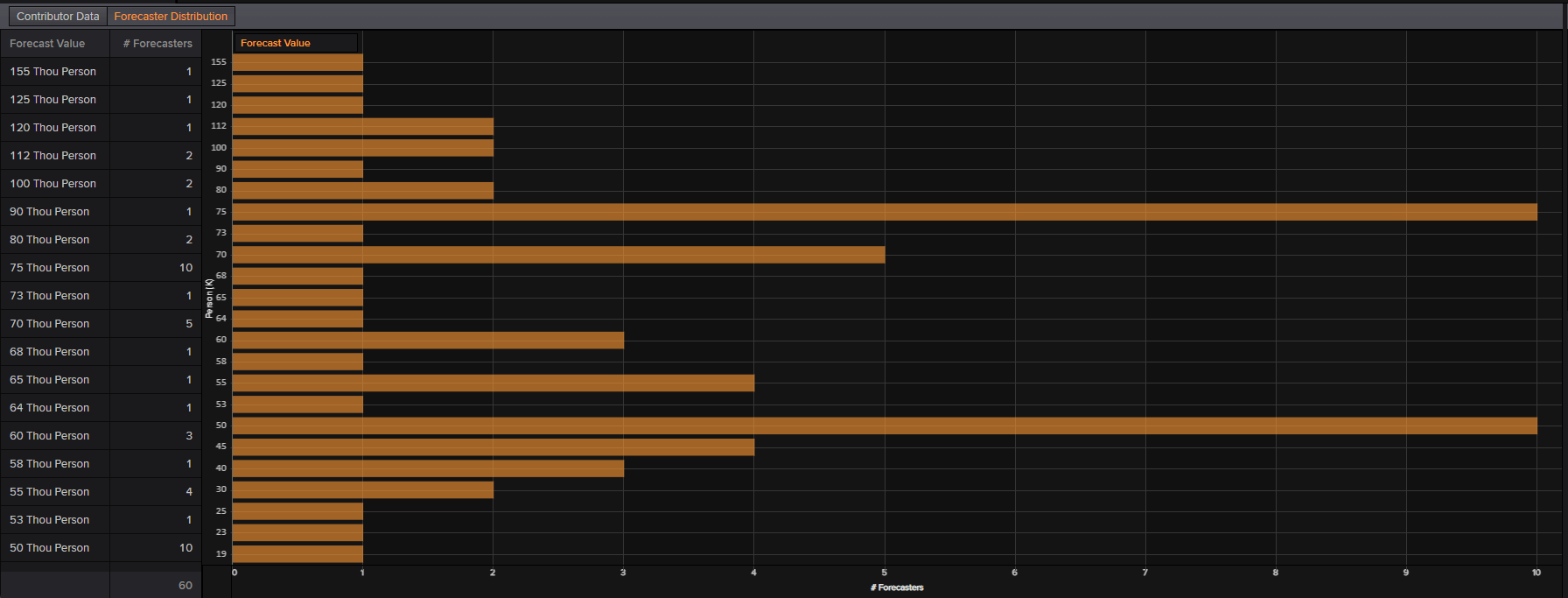

According to the LSEG calendar below, the median estimate for today’s headline payrolls report indicates the US economy added 60,000 jobs, down from 64,000 in November. Based on my research, I believe the market’s whisper number is lower, at around 50,000. As I noted in the previous post, the payroll estimate range is also wide, spanning a high of 155,000 and a low of 19,000, suggesting that economists are uncertain heading into this print.

According to the LSEG calendar below, the median estimate for today’s headline payrolls report indicates the US economy added 60,000 jobs, down from 64,000 in November. Based on my research, I believe the market’s whisper number is lower, at around 50,000. As I noted in the previous post, the payroll estimate range is also wide, spanning a high of 155,000 and a low of 19,000, suggesting that economists are uncertain heading into this print.

The unemployment rate is expected to have ticked lower to 4.5% from 4.6%. Remaining at 4.6% or rising further would be concerning, signalling to the Fed that the jobs market remains a clear problem and a priority for the central bank. At 4.5%, however, I believe this number would give the Fed more time and delay policy easing until later this year.

Per the current forecast distribution below, any payroll number above 100,000 would be sufficient to remove a Fed rate cut from the table in January and significantly reduce the likelihood of a March cut. Nevertheless, at or below 30,000, the January and March meetings would come into focus.

With money markets assigning only about a 12% chance of the Fed cutting rates this month, unless we see some very weak numbers today, it is likely that the Fed will stand pat. March’s meeting is currently pricing in around a 40% probability that the Fed will lower the rate. This will naturally change as the weeks roll on, as we will have much clearer data to work with, with January and February figures released before March’s decision, along with three additional inflation reports.

Also, as a reminder, the market expects the Fed to cut rates twice this year (currently -55 bps), whereas its latest projections (SEP) show just one rate cut.

Publication date: