First Light News: Tariffs, rate decisions, and inflation: Your week ahead brief

The week that WAS

Well, what a week it has been. And that is putting it mildly.

Well, what a week it has been. And that is putting it mildly.

Thanks to US President Donald Trump’s 10% tariff threats against European allies over his Greenland ambitions – sparking the prospect of a fresh trade war – investors rushed for cover and triggered a familiar ‘Sell America’ trade last week. Stock benchmarks, Bonds, and the USD sold off in tandem – a trifecta of misery reminiscent of last year’s ‘Liberation Day’ tariff debacle.

However, just as quickly as storm clouds gathered, they cleared. TACOs were back on the menu, with the President pulling back on the proposed European levies and stating that he will not take Greenland by force. Frankly, I did not expect such a rapid pullback on the tariff threats.

Trump’s speech at the World Economic Forum in Davos, Switzerland, had something for everyone. This consisted of at least 30 minutes of him talking about how great he is to insulting French President Emmanuel Macron’s sunglasses, and ultimately the tariff pullback and his comments regarding his desire to acquire Greenland without the use of military force. Expectedly, this provided a relief rally for risk assets.

The week that IS

Fortunately, for those of us nursing their geopolitical-induced headaches, this week offers a chance to refocus on central bank decisions, inflation figures, and corporate earnings.

Fortunately, for those of us nursing their geopolitical-induced headaches, this week offers a chance to refocus on central bank decisions, inflation figures, and corporate earnings.

Coordinated effort between the US and Japan?

Before I get to that, intervention vibes out of the BoJ are making the airwaves. Despite Friday’s USD/JPY selloff – down 1.7% – this was not an intervention as it was just too small. There have been talks of ‘Fed rate checks’. To be clear, this does not involve buying or selling – it is essentially the Fed contacting dealers to obtain prices they would quote for large orders.

To sum it up, it was this news that sent the USD south, as investors digest a more coordinated approach between the US and Japan, which could lead to larger moves lower. Therefore, keep a close eye on this market!

Fed to hit the pause button, but for how long?

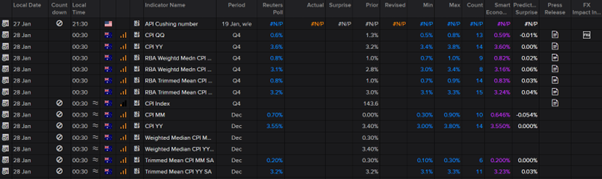

Back to the week ahead, Wednesday will be the highlight of the week for the macro space, delivering updates from the Fed and the BoC – both of which are forecast to remain on hold – and the widely anticipated Australian Q4 25 CPI inflation print.

Publication date: