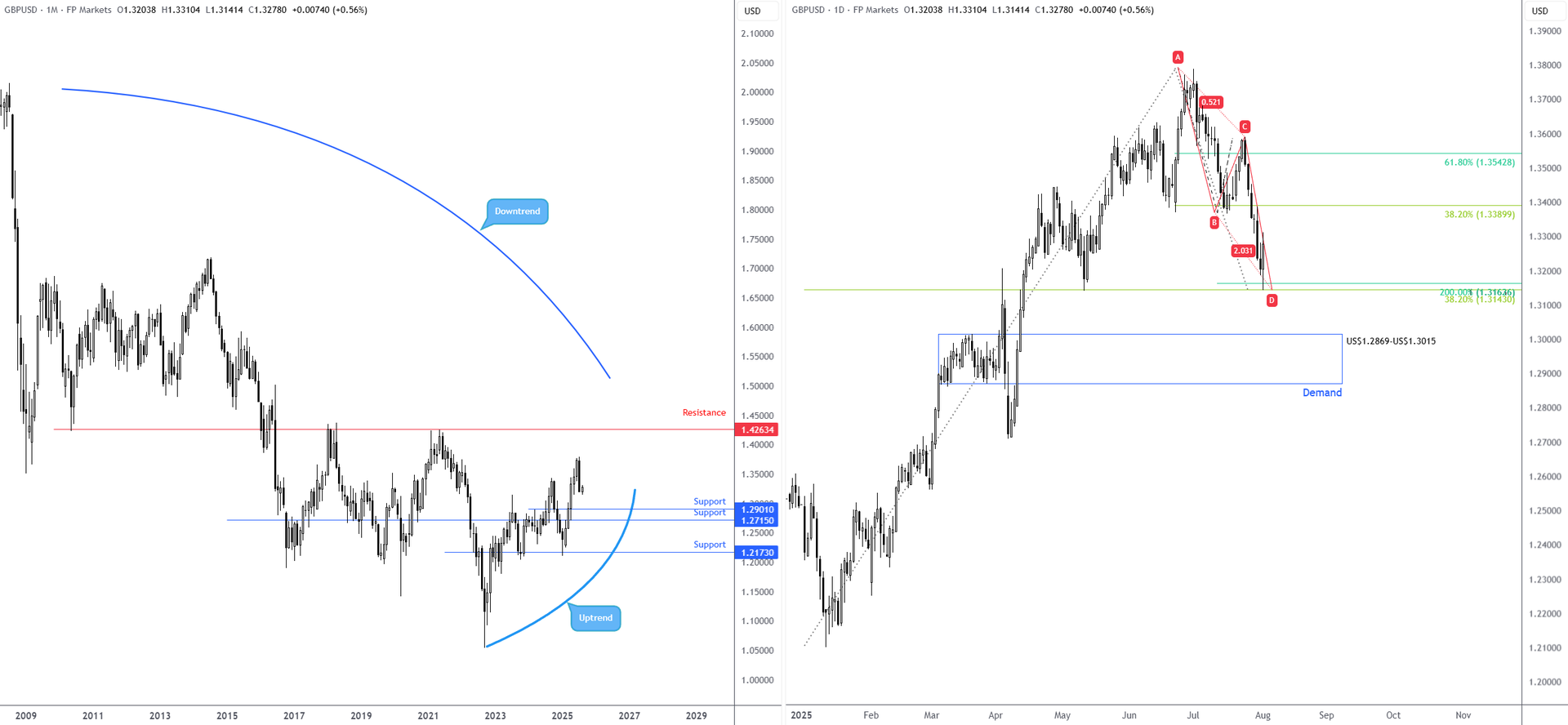

US payrolls surprise to the downside following Fed holding ground; BoE on course for another quarter

Before we dive into the key event of the week, the downside surprise in the July US payrolls data deserves note. The release offered market participants a clear-cut opportunity to trade out of, which, let’s face it, has been few and far between of late, given global uncertainty surrounding US President Donald Trump’s tariffs.

The US dollar (USD) and, in particular, the front end of the yield curve, tanked following the release of the jobs numbers. The 2-year US Treasury yield immediately fell 14 basis points (bps), with investors all but fully pricing in a 25-bp rate cut in September and 64 bps of easing for the year-end. From this, we can see that investors are nearly pricing in three rate reductions from the US Federal Reserve (Fed) this year, meaning we could see rate cuts in September, October, and December. Stocks also finished the week lower, with the S&P 500 and the Nasdaq chalking up weekly bearish engulfing candles and snapping a lengthy winning streak.

Payrolls rose by 73,000, down from 147,000 in June, and from the 110,000 gain forecasted. A look at previous data will show you that this is the first softer-than-expected payroll print since March. The chunky downward revisions were key, and essentially chalked up a more pessimistic picture. The report noted that revisions were bigger than usual for May (revised lower by 125,000 from 144,000 to 19,000) and June (revised down by 133,000, from 147,000 to 14,000). This also brought the 3-month average to just 35,000 in total non-farm payrolls, reflecting a considerably slower pace of hiring in the US.

Digging into the data a little more, you will note that ‘Healthcare and social assistance’ saw a gain in July, and it appears to be the only industry supporting the jobs market right now. Without these gains, we would have seen the payrolls fall into negative territory.

The unemployment rate also ticked higher to 4.2% up from 4.1%, as expected, and wages rose both on a month-on-month and year-on-year basis to 0.3% (up from 0.2%) and 3.9% (up from 3.8% [revised from 3.7%]). The labour force participation rate dropped to 62.2% (down from 62.3%), marking the third consecutive monthly drop, suggesting that people are discouraged from seeking work or that they are leaving the workforce.

The weaker jobs data have certainly called into question the Fed’s wait-and-see stance. We have one more jobs report and two inflation reports ahead of the September meeting to contend with, which will be important, but markets are now largely looking to September for a 25 bp rate cut.

Publication date: