Week Ahead: Tariffs and US Data Eyed

Risk-off sentiment dominated flow last week following US President Donald Trump’s reciprocal tariff announcement, an event he described as ‘Liberation Day’. However, while I cannot speak for everyone, many are not feeling so liberated, with forecasts for growth and inflation upended, as well as economists forecasting a possible global recession.

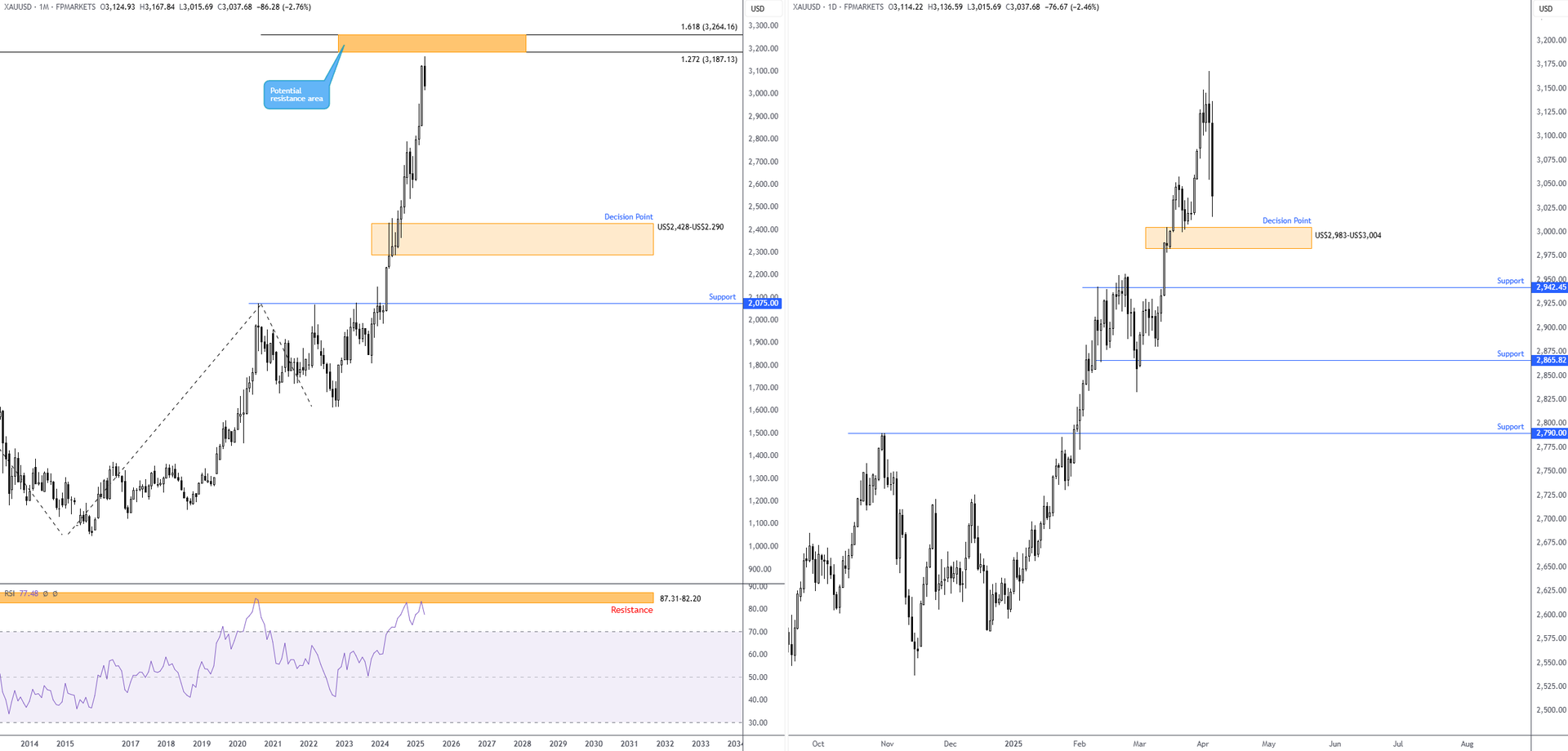

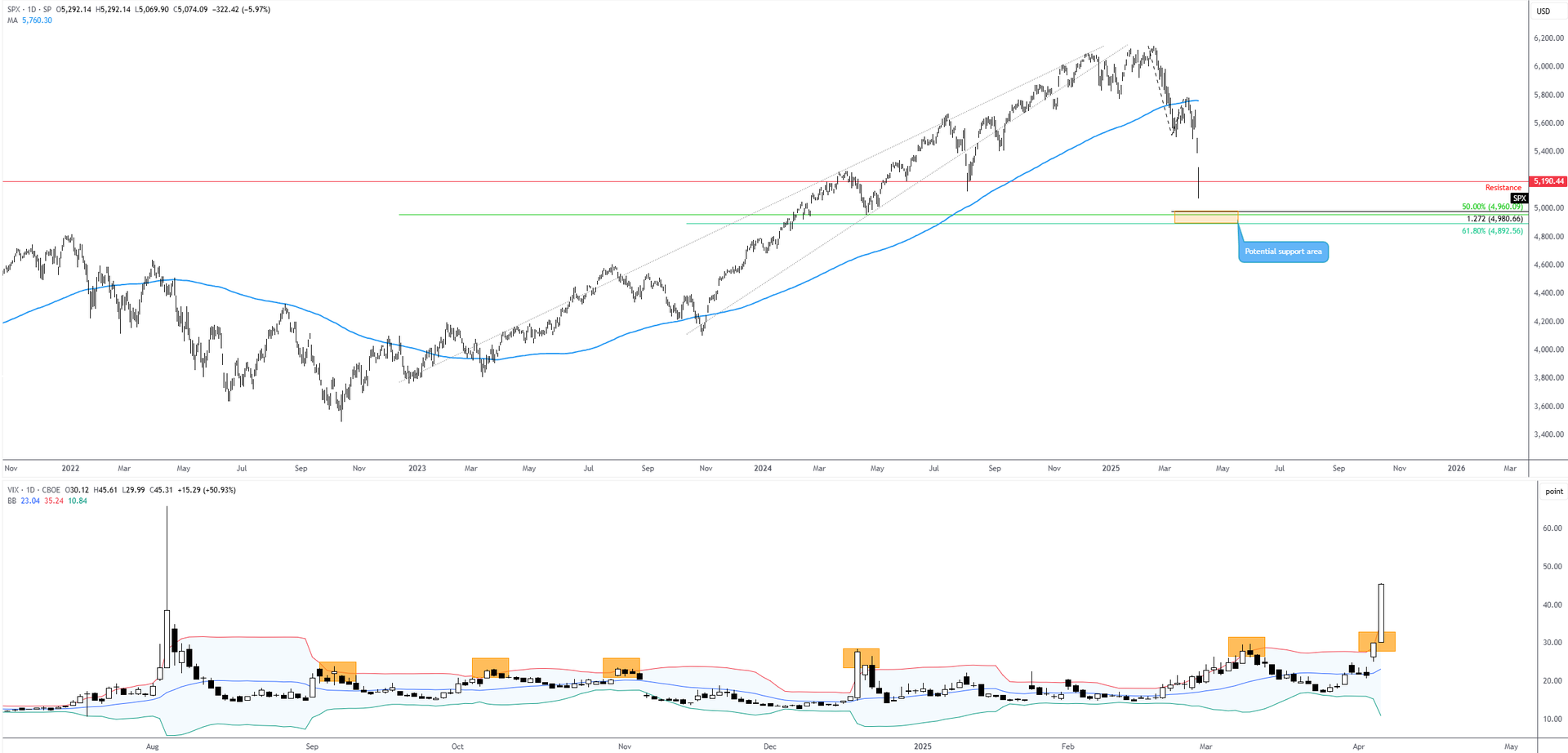

The tariff announcement on 2 April was not digested well by markets, with an evident increase in volatility. Global equities went into freefall and ended the week red across the board, the VIX (Cboe Volatility Index) finished above 45.00 (levels not seen since August 2024), US Treasuries were heavily bid, and the US dollar (USD) closed down 1.4% (per the USD Index), shaking hands with levels not seen since late September 2024, and traditional safe-haven currencies benefitted. In the commodities space, Spot Gold (XAU/USD) explored lower levels from all-time highs of US$3,167, down 1.5%, and WTI Oil (West Texas Intermediate) fell nearly 10%.

Unquestionably, Trump’s ‘Liberation Day’ captivated a global audience. All nations were slapped with a 10% baseline tax on imported goods into the US, which took effect on 5 April. On top of this, higher-than-expected levies were imposed on approximately 60 other countries and are anticipated to go into effect on 9 April, according to a White House Fact Sheet.

The US Employment Situation Report for March was also released on Friday just before the cash open. Despite federal layoffs, 228,000 new jobs were added to the economy, comfortably surpassing the market’s median estimate of 135,000 and 151,000 in February. Despite demonstrating US economic resilience and further highlighting the divergence between hard and soft data, markets were somewhat muted following its release, overshadowed by the global market turmoil from Trump’s tariffs. However, Trump welcomed the latest jobs numbers. He commented via his Truth Social Platform: ‘GREAT JOB NUMBERS, FAR BETTER THAN EXPECTED. IT’S ALREADY WORKING. HANG TOUGH, WE CAN’T LOSE!!!’.

US unemployment ticked slightly higher to 4.2% from 4.1%, with wage growth remaining unchanged at 0.3% month-on-month (MM) and easing to 3.8% from 4.0% year-on-year (YY).

Tariffs; Inflation; Fed Minutes; Consumer Sentiment

In addition to markets closely monitoring US tariff developments this week, particularly responses from trading partners, the macro spotlight will be on US inflation numbers, minutes from the last Fed meeting and consumer sentiment data.

In addition to markets closely monitoring US tariff developments this week, particularly responses from trading partners, the macro spotlight will be on US inflation numbers, minutes from the last Fed meeting and consumer sentiment data.

Publication date: