Week ahead: Bank of England rate cut on the horizon

As global markets head into the second week of May, investors will be closely watching a packed schedule of central bank decisions, key economic data releases, and geopolitical developments.

With US and European monetary policy moves, trade tensions, and oil market dynamics in focus, the week ahead promises important signals for growth, inflation, and market sentiment worldwide. Here’s a snapshot of the notable events shaping the week.

KEY INDICATORS

Central bank decisions in focus

Central bank decisions in focus

- US Federal Reserve (6–7 May): The Federal Reserve is expected to maintain current interest rates at its upcoming meeting, despite political pressure and a recent GDP contraction. Markets are hopeful for potential rate cuts starting in June, especially if inflation continues to ease.

- Bank of England (8 May): The Bank of England is anticipated to implement a 25-basis point rate cut, marking its second reduction this year. This move aims to address low inflation and sluggish wage growth.

- Bank of England (8 May): The Bank of England is anticipated to implement a 25-basis point rate cut, marking its second reduction this year. This move aims to address low inflation and sluggish wage growth.

Key economic indicators

- Monday, 5 May: US ISM Services PMI and S&P Global Services PMI for April.

- Tuesday, 6 May: US trade balance data for March.

- Wednesday, 7 May: Federal Reserve interest rate decision and press conference.

- Thursday, 8 May: US initial jobless claims and labour productivity figures.

- Friday, 9 May: US wholesale inventories and sales data.

- Tuesday, 6 May: US trade balance data for March.

- Wednesday, 7 May: Federal Reserve interest rate decision and press conference.

- Thursday, 8 May: US initial jobless claims and labour productivity figures.

- Friday, 9 May: US wholesale inventories and sales data.

Global market dynamics

- Trade tensions and market sentiment: Recent US tariffs have disrupted global trade, leading to decreased container shipments and concerns over a potential recession. While some progress has been made in trade negotiations, uncertainties remain.

- Oil market outlook: Oil prices have seen modest gains amid expectations that OPEC+ may increase supply. However, the market remains cautious due to ongoing trade tensions and economic uncertainties.

- Oil market outlook: Oil prices have seen modest gains amid expectations that OPEC+ may increase supply. However, the market remains cautious due to ongoing trade tensions and economic uncertainties.

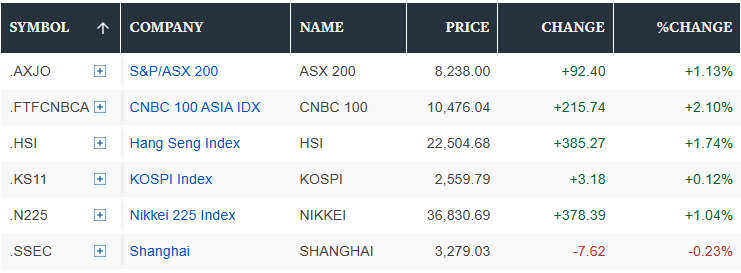

Japanese and Australian stocks rise as Bank of Japan holds rates and most Asian markets close for holiday

Publication date: